This feature story was originally published in the current issue of Photo Review Australia magazine:

In a little over five years, shipments of digital cameras from the Japanese manufacturers have plummeted by 65 percent. Given the word ‘decimate’ means to remove one in ten (ok – it’s a rough translation) then the camera industry has been decimated on an annual basis every year since 2010!

But over the last 12 months or so there have been indications that the good people still involved in the photographic industry after all that decimation are not also on their way to hell in a camera bag. The industry is actually recovering – but it won’t look quite the same when the dust settles and the post-digital revolution industry takes its slightly altered shape.

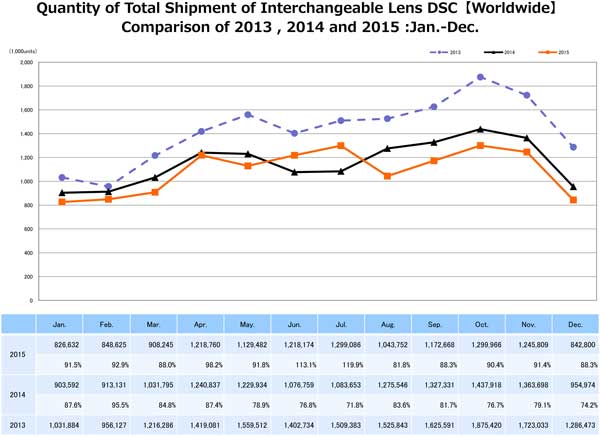

First signs that the downward trend in camera sales was not necessarily permanent came mid-way through last year, when in June and July camera shipments almost matched those of the same months the previous year, and shipments of interchangeable lens cameras actually bettered June and July 2014 by 13 percent and 20 percent respectively.

But one swallow does not a summer make, according to that well known boozer Aristotle, and for the rest of 2015 overall shipments continued to underperform 2014. However, much of the carnage was in the compact camera segment, with interchangeable lens cameras continuing to ship in good, if not stellar, numbers. And even in the compact camera segment, the average selling price of cameras went up as discerning consumers purchased cameras which were more capable than a smartphone – underwater and action models, or superzooms, or premium compacts with large sensors and superior lenses like the Canon G, Ricoh GR the Sony RX ranges.

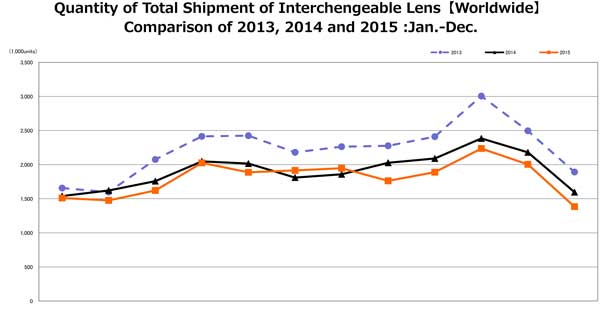

There was also a partial recovery in the accessory lens market, with the biggest improvement in lenses for full-frame sensor cameras, which were up 5 percent in volume terms and 16 percent in value terms. But more of the dynamics of the ‘new’ lens market later.

What we are seeing re-emerge is a camera market more like the one that existed before the introduction of digital cameras in the early years of this century. Digital cameras stopped being a cool and sexy mass market consumer electronics category when smartphones began to replace all those 12-megapixel, 3x and 5x zoom polycarbonate pocket cameras which the likes of Harvey Norman and JB Hi-Fi – not to forget dear old, unlamented Dick Smith – stacked high and sold low for 10 years or so.

This was a punishing era for the friendly local photo store, which wasn’t able to get stock at the same price as the ‘box movers’. Some suppliers – you know who your are – actually made supply at any price problematic for the smaller of their traditional retail customers (ie, they sacked their smallest customers) as they cosied up to their BFFs in the consumer electronics retailing world. Then of course there was the new offshore/online channel – which was particularly challenging when the Australian dollar was at parity with the greenback. Not so much now.

Then there was film – or lack thereof. The biggest economic difference between photo retailing in 2016 and 1996 is that the 32 million rolls of film sold annually in Australia are no longer there. Given a roll of film generated around $30 in purchase price and processing, that’s close to $1 billion which has been taken out of the business. (Looked at another way, photography is $1 billion cheaper than it was 20 years ago!)

The collapse of the ‘snapshooter’ compact market has had an effect on the ‘balance of power’ between specialist and mass merchant/consumer electronics outlets. The CE channel is not so interested in cameras these days, with shelf space shrinking to make way for other categories of products which are more likely to ‘walk off the shelves’ – Fitbits and VR goggles and home espresso machines and the like. This has also had an impact on accessory lines in mass merchants.

The larger retailers rely on sharp pricing rather than any profound product knowledge among staff to make the sale. (A generalisation which some mass merchant Norman photo counter managers and staff could validly dispute.) But as more sophisticated (and expensive) gear represents a larger and tastier slice of the pie, it grows in relative significance for the camera makers, and the photo specialists become more important in their ‘go-to-market’ strategies.

This was noted in positive terms by several high profile retailers we spoke to earlier this year. Jon Paterson, The New Camera House, Lismore, even predicted that as a result of camera distributors re-discovering that their success was linked to specialist retailer retailing skills, the price differentials between the mass marketers and the photo specialists would shrink: ‘Crystal ball prediction for 2016 is we will see a considerable reduction in the gap between the highest and lowest price in the market,’ he noted.

Changing of the guard

Back before digital imaging replaced analog, there was the Big Five in cameras – Canon, Nikon, Olympus, Pentax and Minolta. Though Minolta is no longer with us as a camera brand, Olympus and Pentax are still well in the game, and have been joined by three new camera makers with a consumer electronics heritage: Panasonic, Sony. And Samsung.

Canon and Nikon in the digital era consolidated their place at the top of the totem poll (to the extent that the term ‘Canikon’ is sometimes disparagingly used to describe them.) But they are being challenged like never before. Olympus and Panasonic have done the hard yards with the specialists to win their trust and convince them that the cameras they offer are well worth recommending to customers.

A tale of two marques

The relative fates of Sony and Samsung warrant comparing and contrasting: Both companies are heavy hitters in consumer electronics. Both made a big move into the enthusiast segment of the camera market in 2015 – relatively foreign territory. Both had leading edge camera technology to talk to enthusiasts about – Samsung with its superb NX1 and NX500 and Sony with its equally impressive Alpha mirrorless range and premium RX compacts.

Margaret Brown gave the NX1 a nine-out-of-ten, Editors Choice in Photo Review, concluding: ‘…In the NX1 the company has created a camera that is technologically superior to equivalent DSLRs from the long-time market leaders, Canon and Nikon.’

The NX1 project was three years in development from concept to delivery, according to Samsung Australia’s head of Digital Imaging, Craig Gillespie, with a brief that ‘it had to be the best of the best’.

‘The NX1 camera represents latest pinnacle of Samsung’s research, development and innovation in photographic technology,’ he said.

– But after doing all the hard design and manufacturing work, Samsung seems to have adopted an arrogant ‘we’ve built it – the reviews are great – they’ll come’ attitude, neglecting to take into account the influence of specialist staff on buying decisions.

Samsung’s communications challenge was twofold: it had to motivate high-end camera buyers to desire the Samsung NX1. It also has to motivate photo retailers and their staff to recommend the NX1 at the ‘moment of truth’ across the counter, when qualified prospects were in their store.

‘The NX1 is head and shoulders above anything else in market,’ said Gillespie at the time of the launch of the NX1. – Which it possibly was. Certainly the best APS-C camera released to that time. But Samsung’s marketing communications performance also had to be head and shoulders above anything else in the market if the NX1 was to win pride of place on the shelves, and in the hearts, of photo retailers around the country. It didn’t happen.

On the other hand, Sony had product specialists knocking on camera store doors keen to show managers and staff just how good its camera were. Showing rare humility for a proud brand, Sony’s product specialists even had a Sony A7R II body connected to a high-end Canon lens via a Metabones adaptor, to underscore the fact that owning a collection of Canon lenses was no reason not to make the switch to a Sony body. They even had a Metabones adaptor/Sony Alpha body bundle on offer during 2015!

Now it is 2016, and with two of the stand-out camera releases of 2015, the indications are that Samsung has abandoned the camera market, while Sony has Canon and Nikon looking over their shoulders. Samsung’s withdrawal from the UK and German has been confirmed, and there wasn’t a camera to be seen at the CES trade exhibition early this year, even though Samsung had one of the largest stands.

When questioned at CES by UK enthusiast magazine Amateur Photographer, Samsung refused to say whether or not it even still makes cameras! In Australia the Samsung Digital Imaging department is not answering its phones and mail directed there is being returned to sender.

See separate story for an update.

Even with genuinely great technology, Samsung has failed abysmally to make an impact on the enthusiast photography segment.

Glass houses

The other big change we are seeing is in lenses. For decades, brands like Tamron and Sigma, Cosina and Tokina used to offer inexpensive, quite adequate accessory lenses, mostly zooms, at attractive prices. They still do, but Sigma first and now Tamron have recently disrupted the market with premium, wide-aperture prime and long tele zooms which were previously the sole province of Canon and Nikon.

‘Market-disrupting’ because once an enthusiast or pro has bought into the Canon or Nikon system, the camera companies could charge monopoly prices on their premium lenses. Of course you could move up to a Zeiss, but that would cost even more.

These new ranges – Sigma calls its premium lenses the ‘Art’ series while Tamron’s top glass is designated ‘SP’ – are going to cause Canon and Nikon some financial grief. They cost between a half and a third of the Canon and Nikon equivalents and based on reviews from all over the world, they are every bit as good and sometimes better.

It’s possible, and logical from a marketing perspective, that Canon and Nikon would take a relatively modest margin on the camera body and make up the difference with lenses at monopoly prices. That’s not going to be so easy now that Sigma and Tamron are in the premium end of the market.

Whatever the case, this greater exposure to free market forces must be good for photo enthusiasts and professionals, and empowering for photo retailers.

– Keith Shipton

Be First to Comment